Top 3 Tips for Checking Fee Safety

(Getty Images)

If you have a checking account with a bank or credit union, do you know what the policies are on fees and overdrafts?

Probably not.

"Consumers are expected to wade through long, confusing documents and may be subject to steep, unexpected fees to access their own checking accounts," said Susan Weinstock, director of the Pew Safe Checking in the Electronic Age Project.

Confusion is widespread.

"Our latest research shows that the median length of disclosures for a checking account is 69 pages long," said Weinstock.

The forms are full of fine print and hard-to-read legalese.

"We asked people so what do you do with those papers that the bank gave you when you opened a checking account, and they said we put it in a drawer and filed it away," Weinstock said. "Nobody read these things."

They're full of legalese and fine print.

A new report called "Still Risky: An Update on the Safety and Transparency of Checking Accounts" finds some fees have increased, and that there's been little improvement on disclosures to consumers since the last report in 2010.

Pew found that policies and fee information are not summarized in a uniform, concise, and easy-to-understand format.

"What we found is that consumers really need a disclosure box," Weinstock told ABC News. "What we are pushing is like a nutrition label."

This would make it much easier for consumers to compare their banks' checking and overdraft policies with other firms.

"You'd be able to look at accounts beyond banks and within banks, and decide this is the account that best meets my needs based on the terms the conditions and fees that suit you."

"Seven banks have adopted the box," she said. "Two of the biggest are Chase and TD Bank and we've had two of the three biggest credit unions - Pentagon Federal and North Carolina State Employees Credit Union."

ABC News' checking tips for consumers:

1. Learn what checking fees your bank charges by doing some research.

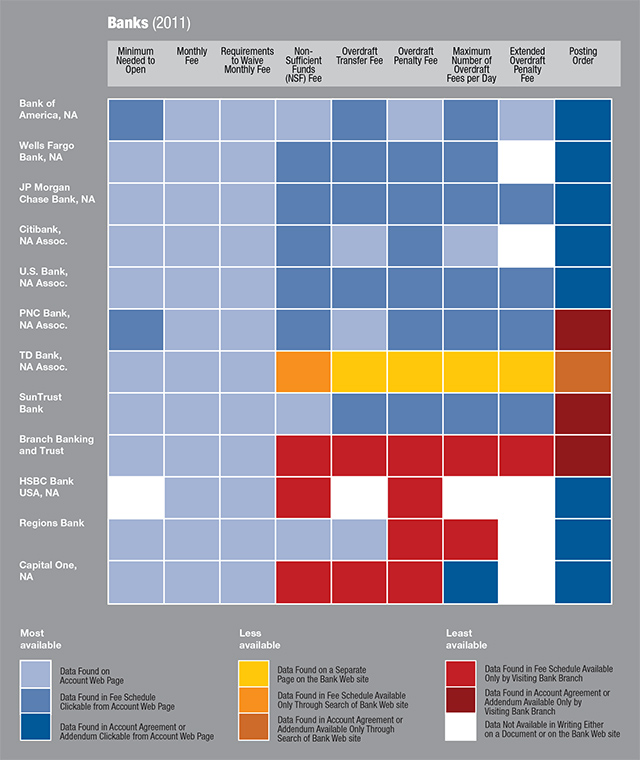

Pew measured the transparency of the 12 biggest U.S. banks by deposit volume and found that some checking information was not disclosed in writing by banks or on their websites. For example, information about extended overdraft penalty fees were not obtainable from Wells Fargo, Citibank, HSBC Bank, Regions Bank and Capital One.

{kind=link}

2. Beware of transaction reordering.

Many banks reserve the right to change their posting order at their discretion, posting withdrawals before deposits in customer accounts and thereby increasing the likelihood of greater overdraft charges. However, four banks in Pew's report disclosed that they post either chronologically or in low-to-high order for at least some types of debits: BB&T, Chase, Citibank and Wells Fargo.

3. Know that protective regulation may be coming, but it's not here yet.

The Consumer Financial Protection Bureau opened a request for information on banks' overdraft practices in February 2012.

Weinstock said Pew is planning to submit its checking safety report this month before the Consumer Financial Protection Bureau stops receiving comments from the public by the end of this month.

"We think that's a great first step and hope it's a step toward writing a rule on the policy recommendations we put forward," she said.