What to know about a global minimum tax rate as 130 nations reach historic agreement

Some 130 countries have agreed to a 15% global minimum tax rate.

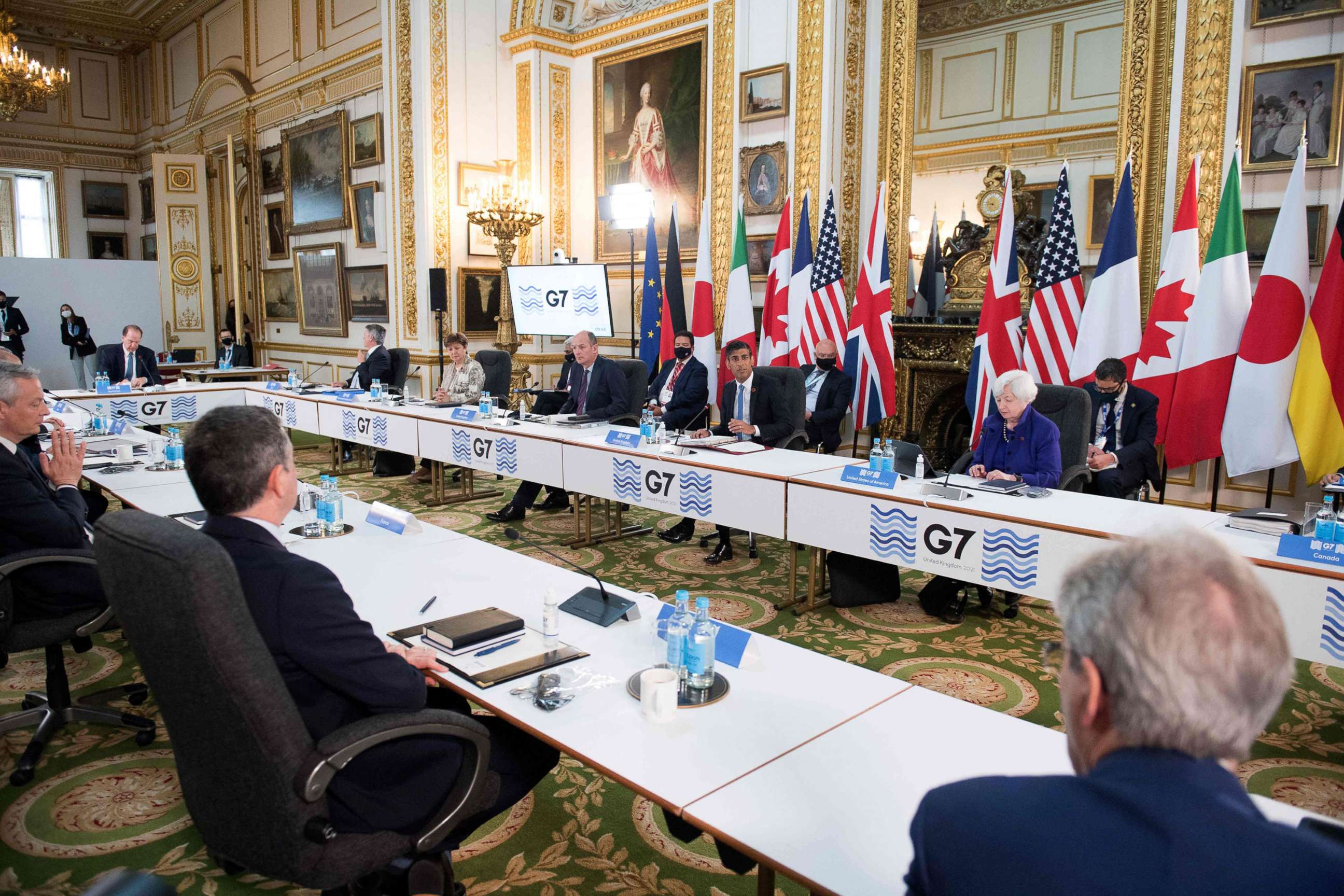

President Joe Biden and Treasury Secretary Janet Yellen announced Thursday that some 130 countries have agreed to a new 15% global minimum tax rate for corporations.

Yellen called it a "historic day for economic diplomacy" in a statement, adding that Biden "has spoken about a 'foreign policy for the middle class,' and today's agreement is what that looks like in practice."

While the agreement was signed by finance ministers from all of the Group of 20 nations and some 130 in total, representing more than 90% of global GDP, it still needs to make it through the legislative bodies of each country -- meaning it's far from a done deal.

Still, the news represents one of the biggest potential reforms in international tax policy in decades. Here is what to know about a global minimum tax rate and how it is expected to impact U.S. businesses and workers.

What is a global minimum tax rate?

A global minimum tax rate is the minimum amount large, international corporations have to pay. The aim is to prevent companies from dodging tax payments by relocating operations or headquarters to another nation with lower rates.

In the U.S., the corporate tax rate is 21% due to former President Donald Trump's 2017 tax cuts, which were implemented in an attempt to keep businesses from fleeing to nations with lower rates. Biden has proposed raising it to 28%.

Ireland, meanwhile, has a corporate tax rate of just 12.5% as part of its own bid to attract business, often at the expense of other European Union nations. Ireland was not listed among the 130 signatories of Thursday's agreement that was arranged by the Organization for Economic Co-operation and Development.

Why a global minimum tax rate?

The OECD estimates that some $240 billion is lost annually to tax avoidance by multinational companies.

Biden said a minimum rate would help prevent companies from exploiting loopholes, with Yellen noting the additional funds collected could be used to help the middle class in areas including education.

"Multinational corporations will no longer be able to pit countries against one another in a bid to push tax rates down and protect their profits at the expense of public revenue," the president said in a statement Thursday. "They will no longer be able to avoid paying their fair share by hiding profits generated in the United States, or any other country, in lower-tax jurisdictions."

Yellen said in a separate statement that the "global race to the bottom" as nations compete to lower their tax rates has "deprived countries of funding for important investments like infrastructure, education, and efforts to combat the pandemic."

Enforcing a 15% minimum tax rate among nations who agree to the plan could generate $150 billion in additional revenue, according to OECD estimates. Moreover, the agreement would provide additional benefits through ensuring stability and certainty for taxpayers and governments.

Advocates, especially in the private sector, have argued that tax competition is beneficial to overall economic growth. The head of the OECD said setting a floor on tax rates doesn't eliminate competition.

"This package does not eliminate tax competition, as it should not, but it does set multilaterally agreed limitations on it," Secretary-General Mathias Cormann said in a statement. "It also accommodates the various interests across the negotiating table, including those of small economies and developing jurisdictions."

When would this happen?

Further details on the plan are expected to be hammered out at the G-20 summit in October, with participating nations targeting 2023 for implementation.

"It is in everyone's interest that we reach a final agreement among all Inclusive Framework Members [139 countries] as scheduled later this year," Cormann said.

Could this lead to further tax reform?

America's labyrinthine tax codes have recently come under scrutiny after a ProPublica report in June unveiled how some of the nation's wealthiest individuals avoid paying taxes on their wealth gains using entirely legal accounting maneuvers.

Although a separate issue, Biden and Yellen signaled that domestic tax reform could be next.

"We have a chance now to build a global and domestic tax system that lets American workers and businesses compete and win in the world economy," Yellen stated.

Biden, meanwhile, called on lawmakers to implement his tax plan that, among other things, raises corporate rates to 28%.

"Building on this agreement will also require us to take action here at home," Biden stated. "It's imperative that we reform our own corporate tax laws, as I proposed in my Made in America tax plan."

ABC News' Sarah Kolinovsky contributed to this report.

Popular Reads

ABC News Live